Repetto Keeps Missing

This morning Sandler O'Neil analyist, Richard Repetto, is once again talking down NYX. He's been talking NYX down since AX days, and has clearly demonstrated that he does not understand the equity market space. Please scroll down to a few posts back with the analysts scorecard to get a sense for how incredibly inaccurate Repetto has been for quite some time.

This morning, Reuters reports that Repetto is citing a potential for a loss in market share as his reason for questioning NYX's growth prospects. You can read this nonsense here.

Market share concerns are nothing new to the NYSE. Click here for a post at NYSE ArcaNews that discusses how market share erosion worries have existed for over 30 years.

Repetto doesn't mention NYSE market share gains in options and ETFs. NYSE market share in these products continues to increase substantially. For example, for the Q's ("QQQQ"), the most heavily traded ETF, NYSE Arca market share is ~33% today. That's roughly 33% greater market share than NYSE did in the Q's trading prior to this month.

ETFs are the mutual fund for the 21st century. Since 1982's codification of 401(k), there's been explosive growth for mutual funds. However, ETFs are slowly making mutual funds obsolete. Here are the numbers (as reported by the Investment Company Institute):

Wayne Gretzky credits much of his success to always trying to play where the puck was headed (click here to read about that). Each day it becomes more evident that the mutual fund puck is headed to ETFs. It'd sure be nice if analysts like Repetto could pick up on these sort of things instead of publishing periodical bear-crap about the potential for market share erosion. But, according to Gretzky, it was his ability to sense and skate to where the puck was headed that seperated him from the pack. It's clear that Repetto isn't all that familiar with that concept.

While on Repetto, it'd be a shame to leave out his claim that the incredible potential of the NYX has already priced into the shares. According to Repetto, the surge from ~64 (AX's last closing price) to levels in the mid-70s is a result of media coverage of the NYX IPO. According to Repetto, at $64 all of the potential for NYX was already baked in.

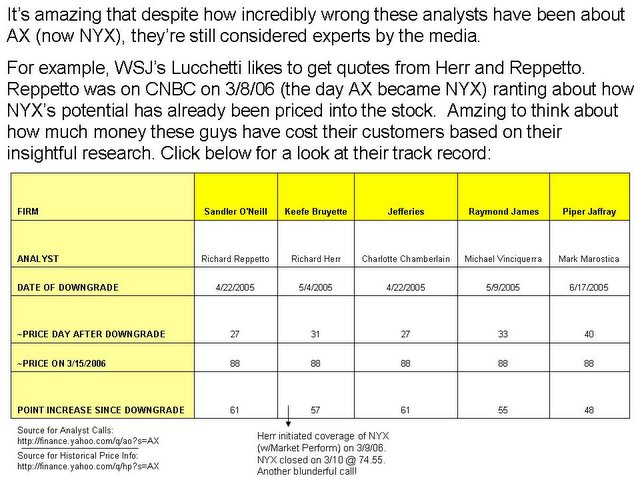

According to Repetto, all of the potential for NYX was baked in when the shares were selling for less than $30. See his downgrade of AX at $27 on 4/22/2006 - just two days after the announced AX/NYSE merger (scroll down to the Analyst Scorecard). Talk about accurate forecasts! Why the media still turns to people like Repetto and Herr for statements is mind boggling.

Market share concerns are nothing new to the NYSE. Click here for a post at NYSE ArcaNews that discusses how market share erosion worries have existed for over 30 years.

Repetto doesn't mention NYSE market share gains in options and ETFs. NYSE market share in these products continues to increase substantially. For example, for the Q's ("QQQQ"), the most heavily traded ETF, NYSE Arca market share is ~33% today. That's roughly 33% greater market share than NYSE did in the Q's trading prior to this month.

ETFs are the mutual fund for the 21st century. Since 1982's codification of 401(k), there's been explosive growth for mutual funds. However, ETFs are slowly making mutual funds obsolete. Here are the numbers (as reported by the Investment Company Institute):

- Total Mutual Fund Assets as of 3/22/2006 = $2.056 trillion (source here)

- Total ETF assets as of January 2006 = $312.79 billion (source here)

Wayne Gretzky credits much of his success to always trying to play where the puck was headed (click here to read about that). Each day it becomes more evident that the mutual fund puck is headed to ETFs. It'd sure be nice if analysts like Repetto could pick up on these sort of things instead of publishing periodical bear-crap about the potential for market share erosion. But, according to Gretzky, it was his ability to sense and skate to where the puck was headed that seperated him from the pack. It's clear that Repetto isn't all that familiar with that concept.

While on Repetto, it'd be a shame to leave out his claim that the incredible potential of the NYX has already priced into the shares. According to Repetto, the surge from ~64 (AX's last closing price) to levels in the mid-70s is a result of media coverage of the NYX IPO. According to Repetto, at $64 all of the potential for NYX was already baked in.

According to Repetto, all of the potential for NYX was baked in when the shares were selling for less than $30. See his downgrade of AX at $27 on 4/22/2006 - just two days after the announced AX/NYSE merger (scroll down to the Analyst Scorecard). Talk about accurate forecasts! Why the media still turns to people like Repetto and Herr for statements is mind boggling.

posted by . at 2:30 PM

1 comments

![]()

![]()